Living on Borrowed Money MacroMonitor Marketing Report Vol. V, No. 10 July 2002

U.S. households are living precariously. Current debt trends indicate that, in the coming years, credit will increasingly become a critical component of a household's financial life, all the way through the retirement stage. For upcoming generations of American consumers, carrying debt will be a normal rite of passage to adulthood and household formation (and a burden that they'll likely carry until they die).

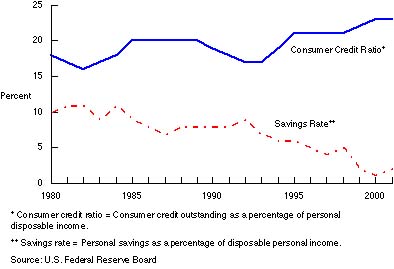

HOUSEHOLD SAVINGS VERSUS CONSUMER CREDIT OUTSTANDING

Analysts in SRI Consulting Business Intelligence's (now Strategic Business Insights') Consumer Financial Decisions (CFD) group expect consumers to take a two-pronged approach in response to the current heavy household debt levels. Some households will view their situation as unsustainable, put the financial brakes on, and start playing safe by saving more, cutting spending, and limiting additional debt. Others will have more difficulty exiting the credit cycle and will continue living on the financial edge.

This two-pronged consumer attitude toward the debt situation has several potential implications for the financial industry:

Analysts in SRI Consulting Business Intelligence's (now Strategic Business Insights') Consumer Financial Decisions (CFD) group expect consumers to take a two-pronged approach in response to the current heavy household debt levels. Some households will view their situation as unsustainable, put the financial brakes on, and start playing safe by saving more, cutting spending, and limiting additional debt. Others will have more difficulty exiting the credit cycle and will continue living on the financial edge.

This two-pronged consumer attitude toward the debt situation has several potential implications for the financial industry:

- Insurance products–not just life insurance, but also disability, credit, and long-term care insurancewill find a receptive market among households that need to secure their financial health.

- Financial planning, particularly retirement planning, will increasingly focus on debt management and the importance of emergency cash reserves, because fewer households will be entering retirement debt free.

- Low-risk savings products will see a resurgence as consumers save rather than invest.

- Nontraditional lenders will likely increase their market share as more financial institutions tighten credit and shift away from subprime lending.