Trends Newsletter June 2022

If you would like more information about this topic, please contact us.

Money on the Move

Every year, money moves within a household (HH) or from one HH to others by way of inheritance. The number of people who will inherit, and how much they will inherit, depends on two basic projections: how many people with money will die, and how much—if any—money they will have when they do.

In the 1950s, with the middle class firmly established, a fairly predictable pattern of money movement prevailed. Men married and went to work; women married and stayed home to raise children. At age 65, the "official" retirement age, white-collar men were able to retire because they had an employer pension plan or social security benefits. At retirement, the man received a gold watch, lived another 10 years (on average), and died. The wife inherited the husband's assets, except when assets were large enough to divvy up between the wife and children/grandchildren. Rarely did the wife have any assets or financial relationships of her own. Bankers of the day were always keen to swoop in on "wealthy widows" to get their assets under (their) management.

By the late 1970s, the first wave of Baby-Boomer women swelled the workforce. The promise to "have it all"—a job, their own money, and children—was espoused. At the turn of the 21st century, women made up 47% of the US workforce. Subsequently, there has been a dramatic increase in women-headed HHs, fueled by delayed marriage (or no marriage) and high divorce rates among 50-something Boomer women. The standard 50/50 divorce settlement is often punitive to mature women who, in order to receive a truly equitable settlement, are rarely advised to employ a financial professional to learn what the HH owns, owes, and earns. When the time comes to move money to the next generation, women's losses—the result of the wage gap, the "mommy penalty," or divorce—will be reflected in the amount of money available for inheritance because most women will need what money they have to live on. Beginning now, there are fewer women than previously without their own financial relationships in place. Most wealthy Boomer widows will know exactly what to do, and who to go to manage their assets.

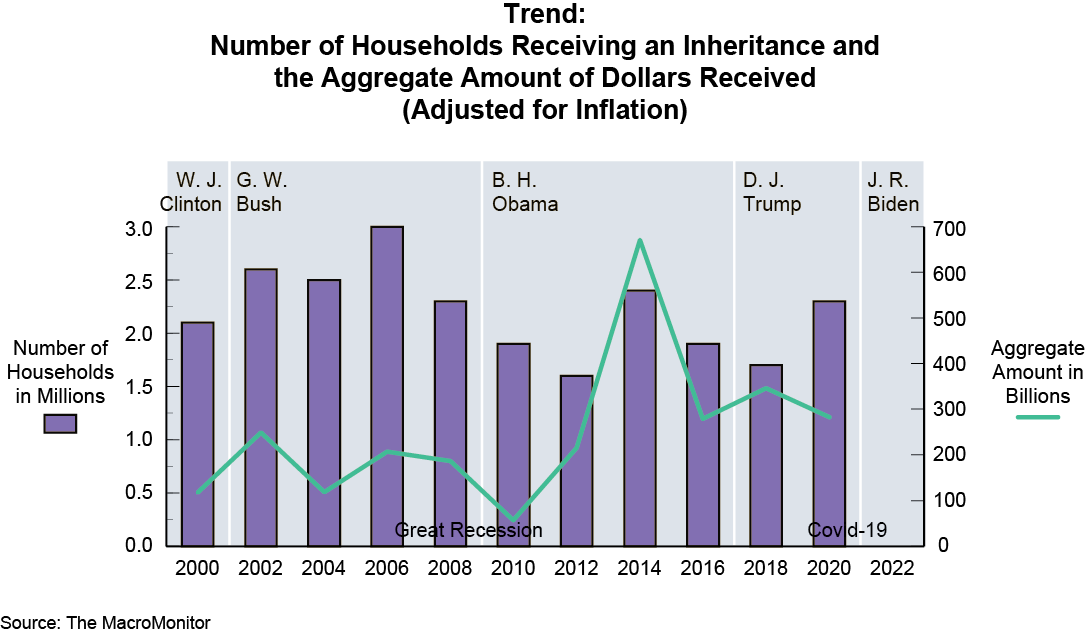

The MacroMonitor reports that the proportion of HHs experiencing the death of a spouse, parent, or other close relative in the past 2 years has declined from 16.4% of HHs in 2000 to 7.7% in 2020. This proportion will increase over the next few years due to the pandemic. As the figure above shows, in 2006, roughly 3 million (2.4%) of all HHs reported inheritance as a source of income; $207bn (adjusted for inflation) was moved. In contrast, in 2014, while only 2.4 million (1.8%) of all HHs had an inheritance income, $671bn was in motion. At least some HHs that inherited in 2014 received more money than HHs did before, or since (2014 was at the peak of the Older-Boomer cohort's presence in the population).

In 2022, the oldest US Boomers turn age 76 and the youngest reach age 60. According to United Nations projections (without factoring in Covid's impacts), the average life expectancy in the US is age 79 (for men, age 77). Over the next decade, the US Census Bureau projects a historic increase in the number of deaths each year due to the sheer size of the Baby-Boomer cohort; "more than 3.6 million [deaths] in 2037, 1 million more than in 2015." The upward trend in deaths will peak in 2055 before gradually leveling off. Even though Boomers have more assets than other cohorts, it's difficult to estimate the amount of money that will be on-the-move. The amount of inheritance assets available will be determined by inflation, how many years Boomers will need their assets to live on, the amount of debt to be paid off, and how much money will be consumed by healthcare costs. Ultimately, the amount received will be determined by state inheritance-tax law. For Baby Boomers who might afford a retirement home, the National Library of Medicine points out that living on a cruise ship provides better amenities, better food, more personalized attention, qualified medical staff available 24/7, and professional entertainment, than do most retirement homes for the same, or less, money. Anticipating costs of their last years, HHs with heads in their 70s are the most likely of all HHs to expect to spend most of their wealth before they die.

Over the course of the next decade, trillions of dollars are likely to be on-the-move. Financial institutions interested in profiting from this money in motion need a strategy to retain current customers' assets and attract assets from competitors. We have insights and expertise to help you. Be in touch to learn more about retaining and attracting assets. Only with a complete understanding of the HHs moving money and the needs of HHs that will most likely be inheriting money, will you be positioned to benefit from the increasing money flows of the next decade.

Contact us to set up a time to Zoom.